Assessing Department

Contact:

Rebel Roberts

Assessing Department

PO Box 38

Canaan NH 03741

603-523-4501, ext. 1030

Office Hours: M-F: 8:30am-4pm

rroberts@canaannh.org

Please also see Office Hours & Closings

Purpose

The Assessing functions are performed by the Assessing Clerk, the professional Assessors and the Board of Selectmen. In addition, the Clerk for Assessing processes timber intent to cut and excavation permits, calculates timber tax and excavation tax; and prepares invoices.

People often ask why the second tax bill is so much higher than the first bill. The first tax bill is an estimate based on last year’s budget and tax base. The actual rate is not set until November of every year. The Town doesn’t receive the amount to be raised by taxes for the County, State and the school until November. Your first bill is usually lower because of that timing. The second bill has to catch up on all of the increases in six months and is therefore twice the increase as the annual tax increase.

Wish to better understand Town Tax Rates? Click here!

Tax Abatements

If you feel you may be eligible, you must apply prior to March 1st for tax abatements, and prior to April 15th for all other requests to be considered for the next tax cycle.

Property Improvements

Before you construct new structures or improvements or additions to existing property, you are required to get a building permit. Failure to get a permit may result in a fine. Call our Building Inspector, at 523-4850 ext. 4 if you have any questions. More information is available on the Building Inspector page.

Tax Assessment

The company of Granite Hill Municipal Services does tax assessment for the Town of Canaan. Appointments are not scheduled, but their vehicles will be marked.

- Taxable properties

- Revaluations

- Appeals

- Exemptions

- Deferrals

- Abatements

- Credits

- Maintaining tax cards

- Maintaining Records of Property Transfers

- Preparation of tax maps

This Assessing Department policy applies when an inspection of private property is required contractually or by directive of the Board of Selectmen.

If a property is posted “no trespassing” or similar but the property access (i.e., driveway, walkway, etc.) is not obstructed by a gate or other objects such as logs or large boulders, the assessing agent will pass and approach the main door of the building to ask permission to complete the assigned assessing related inspection tasks. (Note: This is the same access that is afforded any person conducting routine business (i.e., meter reader, USPS, FedEx, etc.).

If the property owner in unavailable or otherwise does not provide permission for such inspection, the assessing agent will promptly leave the property, but may conduct whatever inspection can be conducted from outside of the property boundaries.

In the event the property is posted “no trespassing” or similar and the property access (i.e., driveway, walkway, etc.) is obstructed with either a gate, large logs or large boulders, the assessing agent will not enter the property.

An assessing agent shall only enter private property when it is safe to do so. The presence of any hazard that may pose a risk of harm to the assessing agent is grounds for the assessing agent to refuse entry.

For purposes of this section, a “hazard” includes, but is not limited to, an unrestrained dog or other animal capable of doing bodily harm, a threatening occupier of the property, or ongoing construction, etc.

- Application for Current Use

- Building Permit

- PA-30: Elderly Tax Exemption Qualifications Worksheet

- Municipal Abatement Form

- Village Tax Stabilization Information & Application Form

- PA-7: Intent to Cut Links:

- PA-29: Permanent Application for Property Tax Credit/Exemptions

The NH Low & Moderate Income Homeowners Property Tax Relief program is designed to lessen the economic burden of the State Education Property Tax on certain at-risk taxpayers.

Criteria

An eligible applicant is a person who is:

- Single with adjusted gross income equal to or less than $37,000; or

- Married or head of NH household with adjusted gross income less than or equal to $47,000; and

- Owns a homestead subject to the State Education Property Tax; and

- Has resided in that homestead on April 1 of the year for which the claim is made.

Filing Period

The filing period begins May 1 of each year and ends June 30.

Application Process

To apply for the NH Low & Moderate Income Homeowners Property Tax Relief program, complete Form DP-8 found on the NH Department of Revenue website, or forms are available at the Canaan Town Hall. Call the Assessing Department at 603-523-4501 ext. 3 to have a form mailed to you.

There are programs created by law to provide property tax credits, exemptions (reduction of the value of taxable property) and deferral of taxes owed. The forms that can be downloaded or filled out on line for these programs can be found at NH Department of Revenue Administration.

- For the Credit & Exemptions, choose PA-29.

- For Elderly & Disabled Tax Deferral use PA-30.

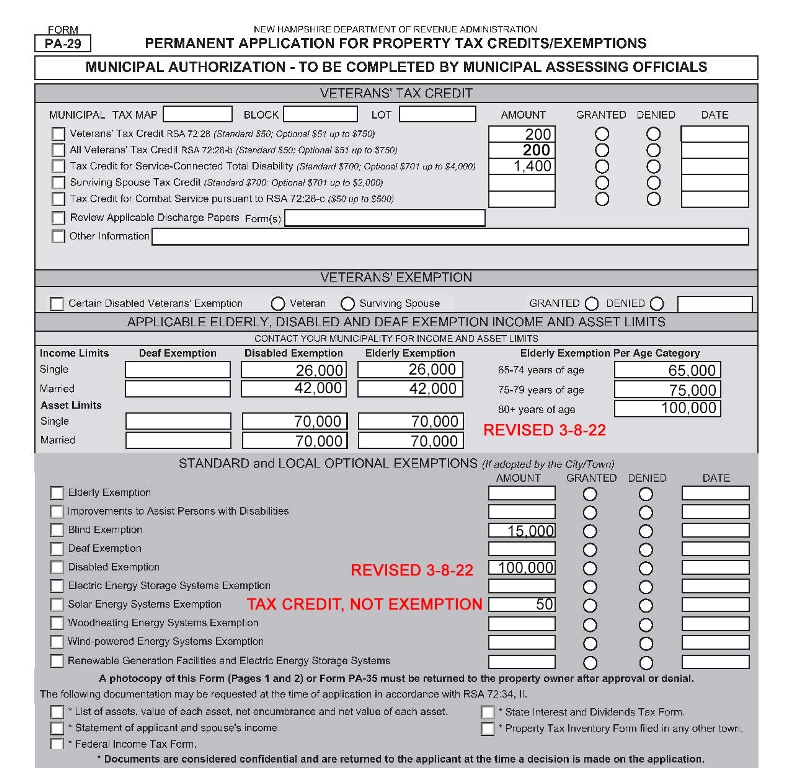

When applying for property tax credits and exemptions, you will need to understand the limitations that apply for each of these programs and these limits will be filled in by the Town.

The limits as approved by the Town voters are shown here:

PDF Version of the Credit Limitations

Downloadable Forms:

The forms that can be downloaded or filled out on line for these programs can be found at NH Department of Revenue Administration.

- For the Intent to cut forms, choose PA-7

- For the Intent to Excavate forms, choose PA-38:

Notice:

If you have filed a Notice of Intent to Cut Wood or Timber for April 1st – March 31st of each year and have not turned your Report of Wood or Timber cut into the Town Offices for processing please do so at your earliest convenience. You have until May 15th of each year to submit your report, after will result in doomage to be charged per RSA 79:12.

Pursuant to RSA 79:12, “If an owner neglects or fails to file a Report of Cut…the assessing officials shall assess to such owner, by way of doomage 2 times as much as such wood and timber would have been taxed had such a report been seasonably filed and truly reported.”

The required forms may have been mailed to the person who did the cutting. The person who did the cutting or the person responsible for the cut who must sign and verify the volumes of the wood and timber reported per RSA 79:11

“The person who did the cutting or the person responsible for the cutting must sign and verify the volumes of wood and timber reported.” Pursuant to RSA 21-J:39 II (c)Criminal Penalties, “No person shall knowingly fail to make a return, report or declaration, which such person is required to do under any tax law.”

If you have any questions please call 603-523-4501 ext 3 or email Ashley Davis at adavis@canaannh.org and she will be happy to assist you.